Investing in your 20s is a smart move that can set you up for a secure financial future. Don’t be discouraged by the misconception that you need a lot of money to start investing. In fact, it’s easier than ever to get started with small amounts of money. Whether you’re saving for retirement, a dream home, or future travel plans, investing early can have a significant impact on your long-term goals. In this article, we’ll share 7 essential tips to help you get started on your investment journey in your 20s.

Determine Your Investment Goals

Before you dive into investing, take some time to think about your goals. Consider the experiences you want to have throughout your lifetime and prioritize them. Do you want to travel every year? Purchase a car in two years? Retire at age 65? Crafting an investment plan tailored to your goals is crucial. Remember to consider your risk tolerance as well. Your 20s are an ideal time to take on some investment risk since you have a long time to recover from any losses. Riskier assets, such as stocks, are often suitable for long-term goals. Once you have a clear set of goals and a plan, you can start exploring specific investment accounts.

Contribute to an Employer-Sponsored Retirement Plan

Saving for retirement may not be a top priority in your 20s, but it should be. By investing in an employer-sponsored retirement plan like a 401(k), you can take advantage of the power of compounding over several decades. Contributions to a 401(k) are made on a pre-tax basis and grow tax-deferred until you withdraw the funds in retirement. Some employers also offer a Roth 401(k) option, allowing tax-free withdrawals during retirement. If your employer offers a matching contribution, be sure to contribute enough to receive the full match. Even if you can’t max out your 401(k) right away, starting small and increasing your contributions over time can make a significant difference.

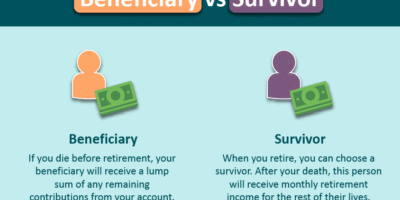

Open an Individual Retirement Account (IRA)

If you don’t have access to an employer-sponsored retirement plan, you can still continue your long-term investment strategy with an Individual Retirement Account (IRA). There are two main types of IRAs: traditional and Roth. Contributions to a traditional IRA are tax-deductible, while qualified distributions from a Roth IRA are tax-free. Experts often recommend Roth IRAs for young investors who are likely in a lower tax bracket now than they will be in retirement. However, it’s important to consider your personal circumstances and consult with a financial advisor to make the best decision for your situation.

Find a Broker or Robo-Advisor

For longer-term goals that aren’t related to retirement, such as a down payment on a future home or education expenses, brokerage accounts are a great option. Online brokers and robo-advisors have made investing more accessible than ever for young people starting with limited funds. These platforms offer low fees, reasonable minimum investments, and educational resources for new investors. Consider using a robo-advisor that aligns with your goals and risk tolerance. They can help you create a portfolio and periodically rebalance it for you.

Consider Leveraging a Financial Advisor

While robo-advisors are a popular choice for new investors, working with a human financial advisor can provide valuable guidance, particularly if you prefer a more personalized approach. Financial advisors can help you establish goals, assess risk tolerance, and find the best brokerage accounts for your needs. They can also provide expert advice on investment strategies and help you navigate the ups and downs of the market. While this option may be more expensive, the expertise and guidance offered can be well worth the cost.

Keep Short-Term Savings Easily Accessible

It’s important to have short-term savings easily accessible and not subject to market fluctuations. This includes your emergency fund and any investments with a short-term use. Savings accounts, certificates of deposit (CDs), and money market accounts are great options for these types of savings. They may not generate high returns like equity investments, but they offer stability and ensure the return of your money when needed.

Increase Your Savings Over Time

Establishing a savings amount that you can stick to and gradually increasing it over time is crucial in your 20s. Committing to a specific savings rate and consistently increasing it each year can have a significant impact on your financial future. Consider automating your savings by setting up automatic transfers from your paycheck to your savings account. To maximize your savings, transfer those funds to a high-yield savings account. By starting early and developing good savings habits, you’ll make it easier to achieve your long-term financial goals as you get older.

Investment Options for Beginners

When starting out as a beginner investor, it’s important to choose investment options that align with your goals and risk tolerance. Here are a few popular options:

- ETFs and Mutual Funds: These funds allow investors to purchase a basket of securities at a relatively low cost, providing diversification for a reasonable fee.

- Stocks: Considered one of the best investment options for long-term goals, stocks can be purchased individually or through ETFs and mutual funds. Thorough research and diversification are key when investing in individual stocks.

- Fixed Income: If you’re more risk-averse, fixed-income investments such as bonds, money market funds, or high-yield savings accounts can be a good starting point. These investments offer lower returns but also come with less risk.

Diversification is Key

To mitigate risk and optimize your investment strategy, it’s crucial to diversify your portfolio. Avoid putting all your eggs in one basket and aim for a mix of different asset classes. By diversifying, you can minimize the impact of any single investment on your overall portfolio and increase your chances of long-term success. Keep in mind that investing in stocks should be done with long-term money, while short-term funds are better suited for cash management accounts or high-yield savings accounts.

Bottom Line

Don’t wait to start investing! Begin by identifying your short-term, intermediate, and long-term goals, and find the right investment accounts to achieve them. While your plans may evolve over time, starting with a retirement account in your 20s is a crucial step to secure your financial future. By investing early, you can harness the power of compound interest and ensure your money keeps up with inflation. Remember, it’s never too early to start investing, and the rewards will compound over time.

Disclaimer: All investors should conduct independent research into investment strategies before making any investment decisions. Past performance is not indicative of future results.